Key Takeaway: The personality of each wave in the Elliott sequence is an integral part of the reflection of the mass psychology it embodies.

The idea of wave personality is a substantial expansion of the Wave Principle. It has the advantage of bringing human behavior more personally into the equation.

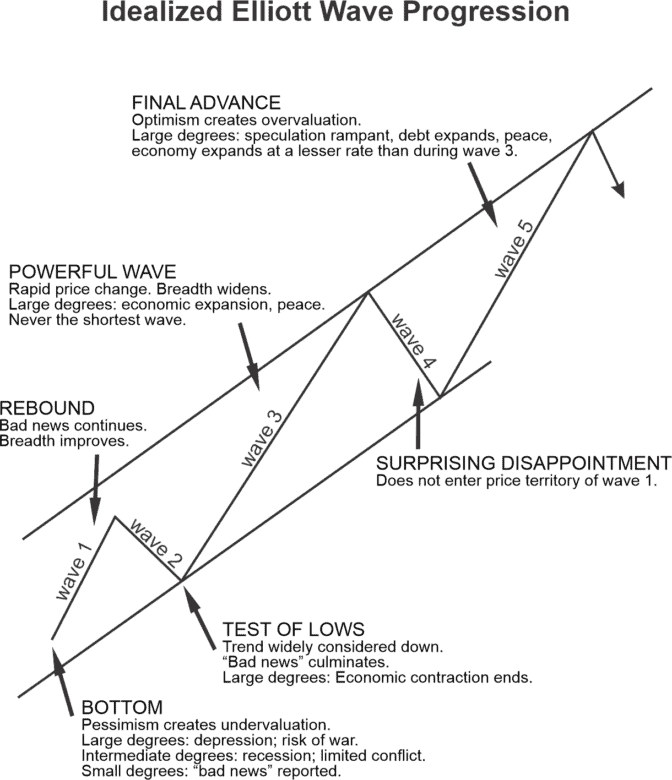

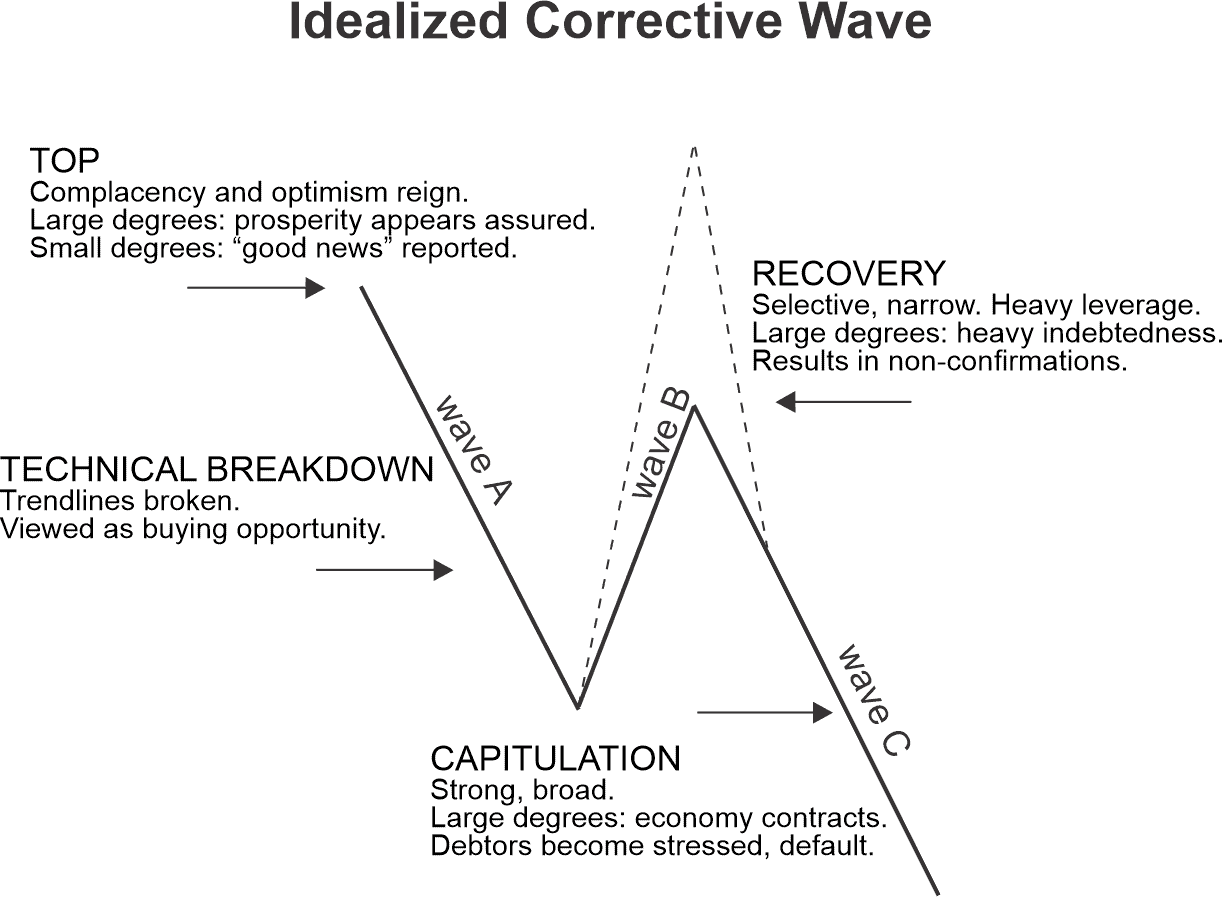

The personality of each wave in the Elliott sequence is an integral part of the reflection of the mass psychology it embodies. The progression of mass emotions from pessimism to optimism and back again tends to follow a similar path each time around, producing similar circumstances at corresponding points in the wave structure. As the Wave Principle indicates, market history repeats but not exactly. Every wave has siblings (same- directional waves of the same degree within a larger wave) and cousins (same-degree and same-numbered waves within different larger waves) but no wave has a twin. Related waves — particularly cousins — have similar market and social characteristics. The personality of each wave type is manifest whether the wave is of Grand Supercycle degree or Subminuette. Waves’ proper- ties not only forewarn what to expect in the next sequence but at times can help determine the market’s present location in the progression of waves, when for other reasons the count is unclear or open to differing interpretations. As waves are in the process of unfolding, there are times when several different wave counts are admissible under all known Elliott rules. It is at these junctures that a knowledge of wave personality can be invaluable. Recognizing the character of a single wave can often allow you to interpret correctly the complexities of the larger pattern. The following discussions relate to an underlying bull market picture, as illustrated in Figures 2-14 and 2-15. These observations apply in reverse when the actionary waves are downward and the reactionary waves are upward.

Figure 2-14

1) First waves — As a rough estimate, about half of first waves are part of the “basing” process and thus tend to be heavily corrected by wave two. In contrast to the bear market rallies within the previous decline, however, this first wave rise is technically more constructive, often displaying a subtle increase in volume and breadth. Plenty of short selling is in evidence as the majority has finally become convinced that the overall trend is down. Investors have finally gotten “one more rally to sell on,” and they take advantage of it. The other fifty percent of first waves rise from either large bases formed by the previous correction, as in 1949, from downside truncations, as in 1962, or from extreme compression, as in 1962 and 1974. From such beginnings, first waves are dynamic and only moderately retraced.

2) Second waves — Second waves often retrace so much of wave one that most of the profits gained up to that time are eroded away by the time it ends. This is especially true of call option purchases, as premiums sink drastically in the environment of fear during second waves. At this point, investors are thoroughly convinced that the bear market is back to stay. Second waves often end on very low volume and volatility, indicating a drying up of selling pressure.

3) Third waves — Third waves are wonders to behold. They are strong and broad. Increasingly favorable fundamentals enter the picture as confidence returns. Third waves usually generate the greatest volume and price movement and are most often the extended wave in a series. It follows, of course, that the third wave of a third wave, and so on, will be the most volatile point of strength in any wave sequence. Such points invariably produce breakouts, “continuation” gaps, volume expansions, exceptional breadth, major Dow Theory trend confirmations and runaway price movement, creating large hourly, daily, weekly, monthly or yearly gains in the market, depending on the degree of the wave. Virtually all stocks participate in third waves. Besides the personality of B waves, that of third waves produces the most valuable clues to the wave count as it unfolds.

4) Fourth waves — Fourth waves are predictable in both depth (see page 66) and form, because by alternation they should differ from the previous second wave of the same degree. More often than not they trend sideways, building the base for the final rise. Lagging stocks build their tops and begin declining during this wave, since only the strength of a third wave was able to generate any motion in them in the first place. This initial deterioration in the market sets the stage for non-confirmations and subtle signs of weakness during the fifth wave.

5) Fifth waves — Fifth waves in stocks are always less dynamic than third waves in terms of breadth. They usually display a slower maximum speed of price change as well, although if a fifth wave is an extension, speed of price change in the third of the fifth can exceed that of the third wave. Similarly, while it is common for volume to increase through successive impulse waves at Cycle degree or larger, it usually happens in a fifth wave below Primary degree only if the fifth wave extends. Otherwise, look for lesser volume as a rule in a fifth wave as opposed to the third. Market dabblers sometimes call for “blowoffs” at the end of long trends, but the stock market has no history of reaching maximum acceleration at a peak. Even if a fifth wave extends, the fifth of the fifth wave will lack the dynamism that preceded it. During advancing fifth waves, optimism runs extremely high despite a narrowing of breadth. Nevertheless, market action does improve relative to prior corrective wave rallies. For example, the year-end rally in 1976 was unexciting in the Dow, but it was nevertheless a motive wave as opposed to the preceding corrective wave advances in April, July and September, which, by contrast, had even less influence on the secondary indexes and the cumulative advance-decline line. As a monument to the optimism that fifth waves can produce, the advisory services polled two weeks after the conclusion of that rally turned in the lowest percentage of “bears,” 4.5%, in the history of the recorded figures despite that fifth wave’s failure to make a new high!

6) A waves — During the A wave of a bear market, the in- vestment world is generally convinced that this reaction is just a pullback pursuant to the next leg of advance. The public surges to the buy side despite the first really technically damaging cracks in individual stock patterns. The A wave sets the tone for the B wave to follow. A five-wave A indicates a zigzag for wave B, while a three-wave A indicates a flat or triangle.

7) B waves — B waves are phonies. They are sucker plays, bull traps, speculators’ paradise, orgies of odd-lotter mentality or expressions of dumb institutional complacency, or both. They often involve a focus on a narrow list of stocks, are often “unconfirmed” (see Dow Theory discussion in Chapter 7) by other averages, are rarely technically strong, and are virtually always doomed to complete retracement by wave C. If the analyst can easily say to himself, “There is something wrong with this market,” chances are it’s a B wave. X waves and D waves in expanding triangles, both of which are corrective wave advances, have the same characteristics. Several examples will suffice to illustrate the point.

— The upward correction of 1930 was wave B within the 1929-1932 A-B-C zigzag decline. Robert Rhea describes the emotional climate well in his opus, The Story of the Averages (1934):

…many observers took it to be a bull market signal. I can remember having shorted stocks early in December, 1929, after having completed a satisfactory short position in October. When the slow but steady advance of January and February carried above [the previous high], I became panicky and covered at considerable loss. …I forgot that the rally might normally be expected to retrace possibly 66 percent or more of the 1929 downswing. Nearly everyone was proclaiming a new bull market. Services were extremely bullish, and the upside volume was running higher than at the peak in 1929.

Figure 2-15

— The 1961-1962 rise was wave (b) in an (a)-(b)-(c) expanded flat correction. At the top in early 1962, stocks were selling at unheard of price/earnings multiples that had not been seen up to that time and have not been seen since. Cumulative breadth had already peaked along with the top of the third wave in 1959.

— The rise from 1966 to 1968 was wave B in a corrective pattern of Cycle degree. Emotionalism had gripped the public and “cheapies” were skyrocketing in the speculative fever, unlike the orderly participation of the secondaries within first and third waves. The Dow Industrials struggled unconvincingly upward throughout the advance and finally refused to confirm the new highs in the secondary indexes.

— In 1977, the Dow Jones Transportation Average climbed to new highs in a B wave, miserably unconfirmed by the Industrials. Airlines and truckers were sluggish. Only the coal-carrying rails were participating as part of the energy play. Thus, breadth within the index was conspicuously lacking.

— For a discussion of the B wave in the gold market, see Chapter 6, page 180. As a general observation, B waves of Intermediate degree and lower usually show a diminution of volume, while B waves of Primary degree and greater can display volume heavier than that which accompanied the preceding bull market, usually indicating wide public participation.

8) C waves — Declining C waves are usually devastating in their destruction. They are third waves and have most of the properties of third waves. It is during these declines that there is virtually no place to hide except cash. The illusions held throughout waves A and B tend to evaporate and fear takes over. C waves are persistent and broad. 1930-1932 was a C wave. 1962 was a C wave. 1969-1970 and 1973-1974 can be classified as C waves. Advancing C waves within upward corrections in larger bear markets are just as dynamic and can be mistaken for the start of a new upswing, especially since they unfold in five waves. The October 1973 rally (see Figure 1-37), for instance, was a C wave in an inverted expanded flat correction.

9) D waves — D waves in all but expanding triangles are often accompanied by increased volume. This is true probably because D waves in non-expanding triangles are hybrids, part corrective, yet having some characteristics of first waves since they follow C waves and are not fully retraced. D waves, being advances within corrective waves, are as phony as B waves. The rise from 1970 to 1973 was wave D within the large wave IV of Cycle degree. The “one-decision” complacency that characterized the attitude of the average institutional fund manager at the time is well documented. The area of participation again was narrow, this time the “nifty fifty” growth and glamour issues. Breadth, as well as the Transportation Average, topped early, in 1972, and refused to confirm the extremely high multiples bestowed upon the favorite fifty. Washington was inflating at full steam to sustain the illusory prosperity during the entire advance in preparation for the presidential election. As with the preceding wave B, “phony” was an apt description.

*****************

10) E waves — E waves in triangles appear to most market observers to be the dramatic kickoff of a new downtrend after a top has been built. They almost always are accompanied by strongly supportive news. That, in conjunction with the tendency of some E waves to stage a false breakdown through the triangle boundary line, intensifies the bearish conviction of market participants at precisely the time that they should be preparing for a substantial move in the opposite direction. Thus, E waves, being ending waves, are attended by a psychology as emotional as that of fifth waves.

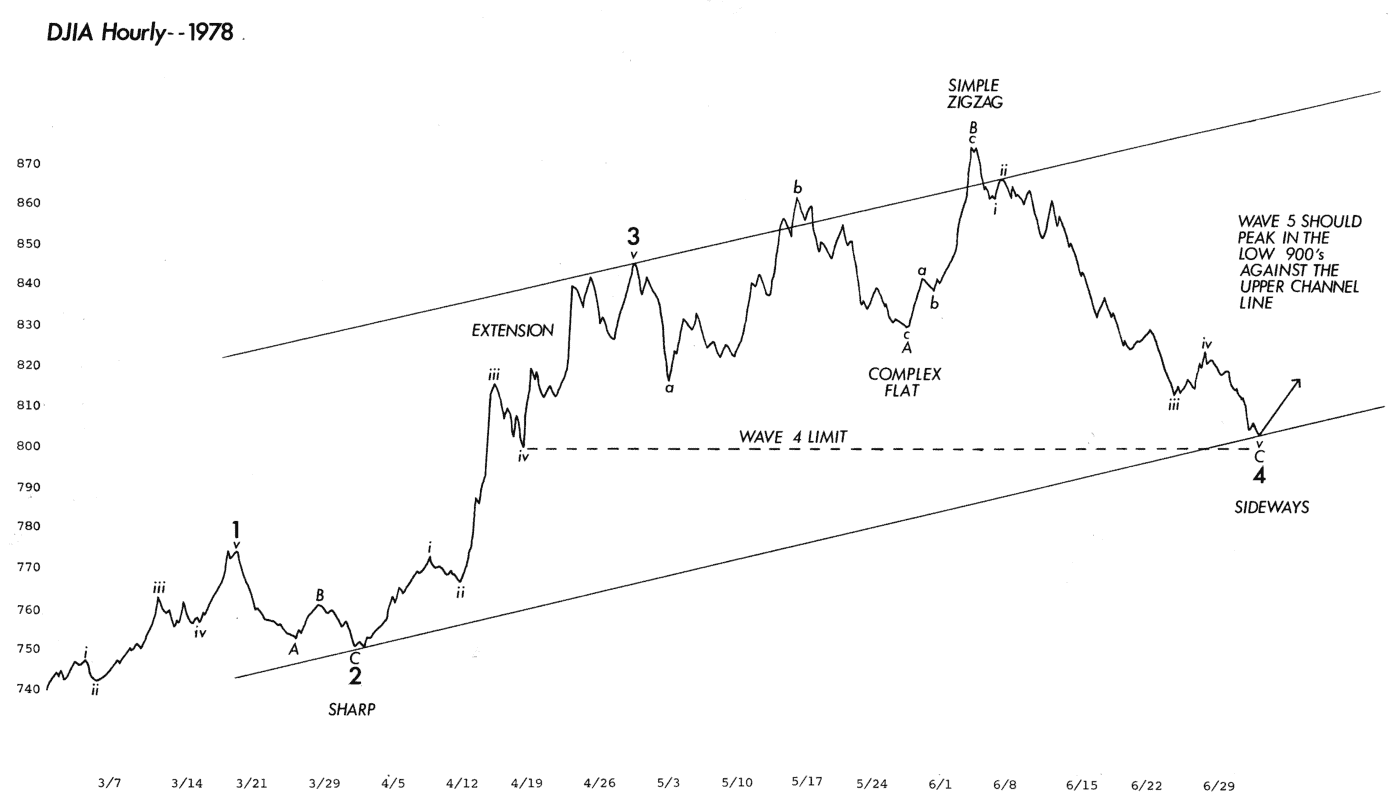

Because the tendencies discussed here are not inevitable, they are stated not as rules, but as guidelines. Their lack of inevitability nevertheless detracts little from their utility. For example, take a look at Figure 2-16, an hourly chart of the most recent market action, the first four Minor waves in the DJIA rally off the March 1, 1978 low. The waves are textbook Elliott from beginning to end, from the length of waves to the volume pattern (not shown) to the trend channels to the guideline of equality to the retracement by the “a” wave following the extension to the expected low for the fourth wave to the perfect internal counts to alternation to the Fibonacci time sequences to the Fibonacci ratio relationships embodied within. Its only atypical aspect is the large size of wave 4. It might be worth noting that 914 would be a reasonable target in that it would mark a .618 retracement of the 1976-1978 decline.

There are exceptions to guidelines, but without those, market analysis would be a science of exactitude, not one of probability. Nevertheless, with a thorough knowledge of the guidelines of wave structure, you can be quite confident of your wave count. In effect, you can use the market action to confirm the wave count as well as use the wave count to predict market action.

Notice also that Elliott wave guidelines cover most aspects of traditional technical analysis, such as market momentum and investor sentiment. The result is that traditional technical analysis now has a greatly increased value in that it serves to aid the identification of the market’s position in the Elliott wave structure. To that end, using such tools is by all means encouraged.

Figure 2-16

“So wait… I can really learn to predict the markets?”

Yes. Markets aren’t rational. For every action, there isn’t always an equal and opposite reaction.

What drives prices isn’t logic, but emotion. Market emotions unfold in predictable patterns called Elliott waves. That’s what makes prices predictable.

What you just read is from the Wall Street bestseller, “Elliott Wave Principle: Key to Market Behavior.” For 40+ years, it’s been a top-shelf book on unbiased market analysis.

Amazon reviewers call it “classic and essential” and “the bible of the theory.” Now, you can get instant, FREE access to the full online version of this book ($29 value).