Don’t Chase Trends. Anticipate Them.

Why would you need a global publication?

Because the world’s biggest opportunities rarely begin in just one market.

Stocks, bonds, currencies, commodities, precious metals, cryptocurrencies and interest rates are all connected. Yet most investors only follow a handful of them—and spend the rest of their time trying to interpret an endless stream of headlines.

Global Market Perspective gives you a broader view.

Each month, our team of 12 specialized analysts steps back from the daily noise to examine more than 50 global markets and identify the larger trends taking shape beneath the surface. Using Elliott wave analysis and socionomic principles, they focus on where opportunities may be emerging, where risks may be growing, and what developments deserve your attention right now.

You’ll receive coverage of U.S., European and Asian stock markets, interest rates, currencies, precious metals, energy markets, cryptocurrencies, commodities and important cultural and social trends that help provide context for what investors are doing—and why.

No single analyst can follow the entire world. That’s why Global Market Perspective brings together specialists who dedicate themselves to understanding their markets full-time and combine their work into this one comprehensive monthly publication.

Together, they’ve helped subscribers navigate speculative manias, financial crises, commodity booms, currency swings and major turning points in global markets for decades.

The result is a publication designed to help you anticipate important trends instead of simply reacting to them.

If you want more frequent updates, add a regional Short Term Update

For investors who want to stay closer to fast-moving developments, our regional Short Term Updates provide concise analysis three times each week.

Whether your focus is the United States, Europe or Asia-Pacific markets, these publications act as a bridge between monthly issues—highlighting important changes in wave structure and keeping you aligned with the market’s evolving outlook.

Subscribe now and get instant access to recent issues, so you can quickly get up to speed on the world’s most important markets.

Meet The Global Market Perspective Analytical Team

View Some Of Our Notable Market Forecasts

For more than 35 years, this publication has identified many bullish and bearish opportunities for its subscribers — often when the crowd was most convinced of the opposite.

Not all our forecasts work out, but we challenge you to find another service this dedicated to getting it right time after time. Here are some highlights:

1994: The Bond Market Crisis / “Great Bond Massacre”

After years of disinflation and falling yields, investors were deeply positioned for stability. Wall Street strategists saw little reason to expect a major bond sell-off.

Analysis/Forecast:

January 1, 1994:

“The bond market topped in October, and is nearing the onset of Minor Wave 3 down, which should be longer and more persistent than wave 1 (Oct–Nov). Canadian bonds should make a final high this month, coincident with a secondary peak in U.S. bonds. All other markets are expected to make important tops as well.”

February 1, 1994:

“U.S. Treasury notes and bonds are ending wave (2), and are about to begin wave (3) down… Most other bonds began declines or consolidations in January, as expected…”

What Happened Next?

By spring 1994, global bond prices collapsed in what became known as “The Great Bond Massacre.” U.S. Treasuries lost more than 10%, and leveraged portfolios worldwide were blindsided — just as GMP’s wave count warned.

2000: The “Dot-Com” Peak

At the height of the technology mania, analysts declared a “new economy.” The Nasdaq’s parabolic surge convinced investors that the boom could not end.

Analysis/Forecast:

February 22, 2000:

“The DJIA’s break of 10,355 confirms that a bear trend started at the 11,750 high of January 14… A third wave is underway… Support is 9375–9575… A significant slice through this lower support increases the odds for a crash.”

“The NASDAQ 100… has been wedging higher since the beginning of the year. Prices have been tracing out an ending pattern called a diagonal … Once an ending diagonal finishes, prices usually decline sharply.”

Interim – March 1, 2000:

“The Dow averages, S&P 500 and New York Composite are now in sync to the downside. The NASDAQ 100 achieved the new high allowed for in our Interim Report but now sits on the cusp of a sharp reversal as the pattern traces out the final subdivisions of its fifth wave. A close beneath 4024 will align this last rising index with the rest of the market and signal the end of the mania.”

What Happened Next?

The Nasdaq topped on March 10, 2000 — within weeks of our warning — and lost 78% over the next 31 months. The S&P 500 and Dow entered a multi-year bear market as the “new paradigm” collapsed.

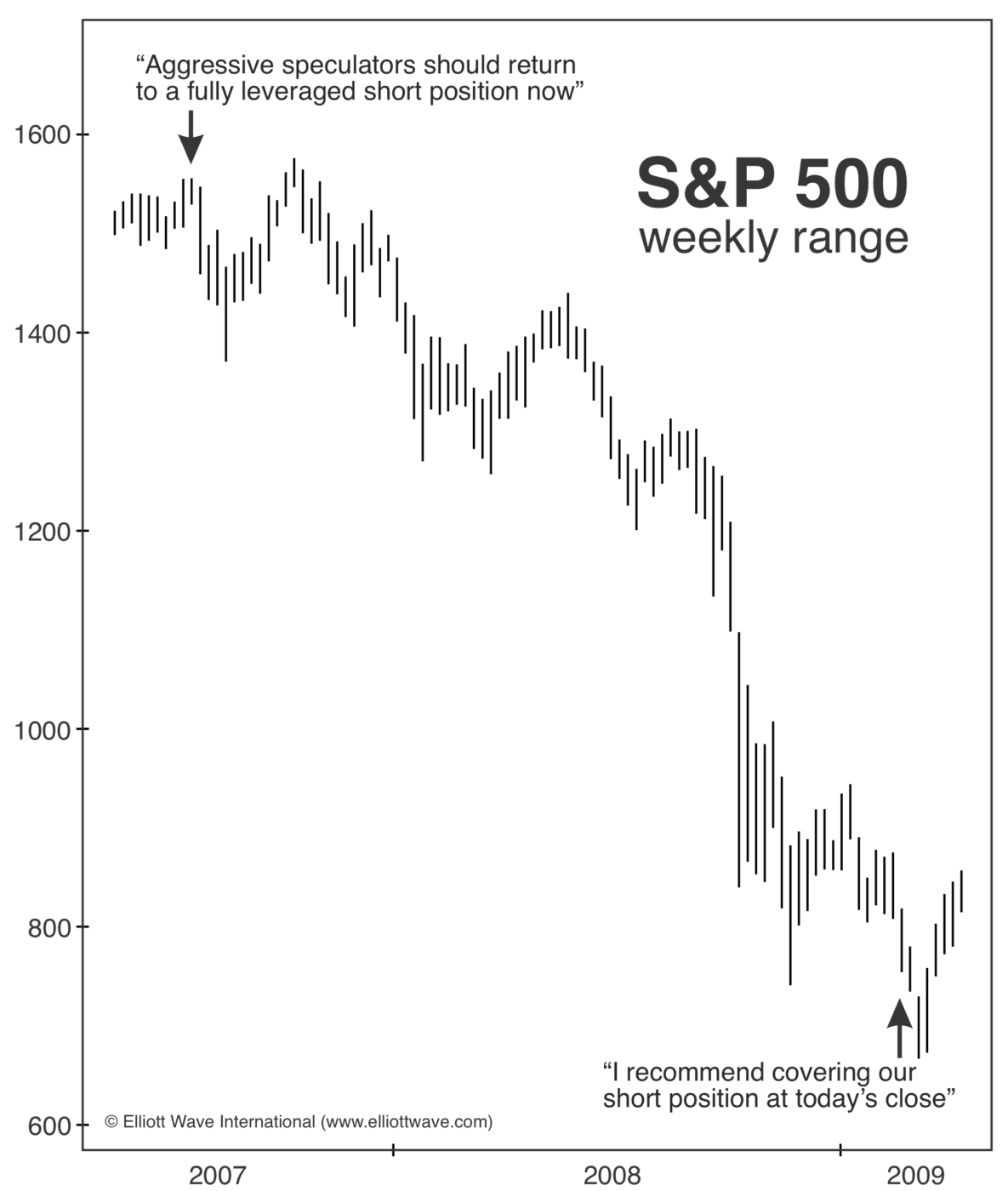

2007 & 2009: The Great Financial Crisis (Calling The Top & the Bottom)

In July 2007, as stocks were still climbing and risks were widely dismissed, The Elliott Wave Theorist warned:

July 17, 2007:

“Aggressive speculators should return to a fully leveraged short position now. We may be early by a couple of weeks, but the market has traced out the minimum expected rise, and that’s enough to act upon.”

Then in August and September, Global Market Perspective told subscribers:

August 1, 2007:

“The transition from the Great Asset Mania to the Great Credit Contraction is confirmed by a turn down in the major stock indexes, which started “the great decline” following one more new high in July, as forecast here last month. Sentiment continues to view the credit bust as specific to the subprime area, but it should be global in scope. Near term, a relief rally may well be starting, but it should hold well beneath the July highs and lead to greater selling pressure.”

September 28, 2007:

“The July 17 Interim Report of The Elliott Wave Theorist identified the DJIA’s top tick to the day and advised a return to a fully bearish stance… the entire rally from 2002–2003 should be complete and bear market back underway.”

After a slight new high in the Dow in October (but not in the NYSE or DJ Composite indexes), the U.S. entered the worst financial crisis since the Great Depression.

Then, in early 2009 — when fear dominated and most expected further collapse — we said this to subscribers:

The Elliott Wave Theorist,

February 23, 2009:

“…over the past four months EWT, EWFF and STU have repeatedly stated, without equivocation, that the market required a fifth wave down. There were no alternate counts. The Wave Principle virtually guaranteed lower lows, and now we have them.

If you are a slick trader, perhaps you can finesse the final waves or snag some more profits early tomorrow. But as for our official position, I recommend covering our short position at today’s close.

Global Market Perpective,

February 27, 2009:

“Some measures of market sentiment are achieving pessimistic extremes, so the decline is likely reaching its latter stages…

Once five waves are complete within wave (5), the odds will be high that a low is at hand.”

Just days after our reports, the market bottomed on March 9, 2009 — launching one of the most powerful bull markets in history.

Our subscribers weren’t reacting to extremes — they were prepared for them.

Here’s the timing of those forecasts in the S&P 500:

An 800-point trade speaks for itself… And now we may be on the precipice of another opportunity.

See What Our Analysts Are Saying Now:

“I’m a subscriber to all of your flagship publications and I find your analysis of the U.S. stock markets, bonds, the dollar and precious metals to be of the highest caliber. You have achieved a level of expertise which is unparalleled in the industry, and your analysis definitely needs to be an integral part of any serious trader’s decision making process.”

– Chester B.

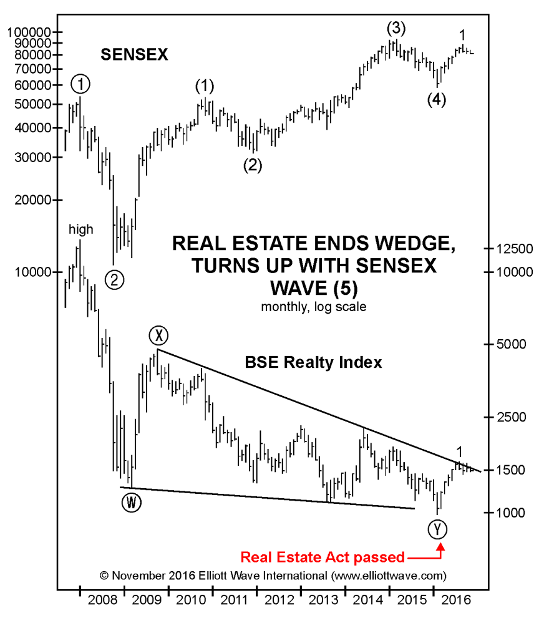

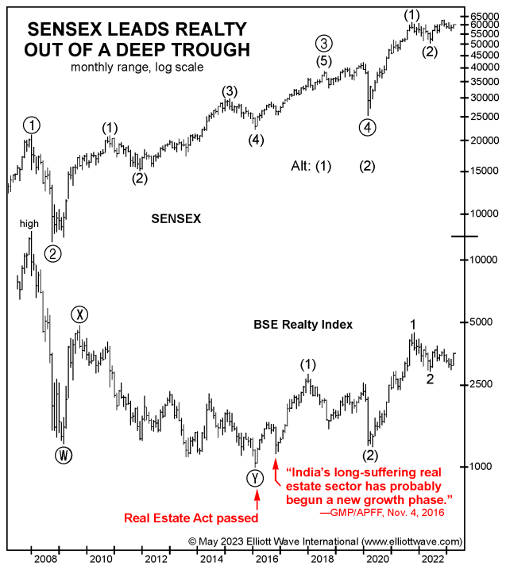

2016: BSE Realty Index

By 2016, India’s real estate sector had endured years of stagnation following the post-2008 downturn. The BSE Realty Index had lost more than 85% from its 2008 peak, and investor sentiment toward property developers remained deeply negative.

However, in March 2016, India passed the Real Estate (Regulation and Development) Act, aimed at improving transparency and restoring confidence to the sector — an important policy shift just as prices were stabilizing near multi-year lows.

Analysis/Forecast:

November 4, 2016:

“India’s long-suffering real estate sector has probably begun a new growth phase.”

What happened next?

The BSE Realty Index went on to more than triple over the next several years, confirming that 2016 marked a major low.

By 2021, the index reached levels not seen since 2011, and India’s property developers entered a sustained recovery period that mirrored renewed strength in the Sensex and the broader economy.

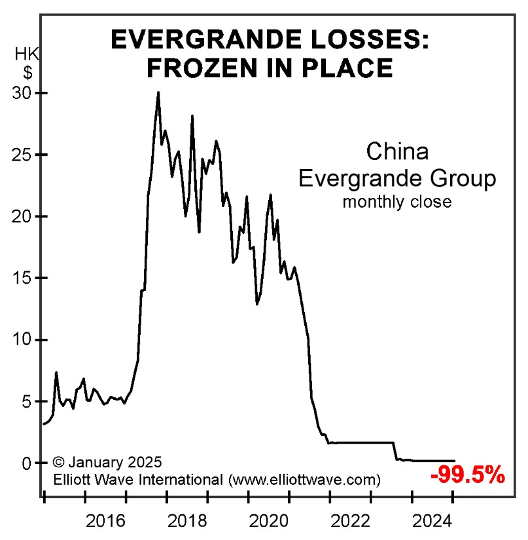

2017: China Evergrande Group

In 2017, China’s real estate boom seemed unstoppable. One real estate development firm towered above the rest: China Evergrande Group. The firm’s rapid growth was aided by overconfidence and huge amounts of leverage.

Analysis/Forecast:

Global Market Perspective –July 2017

“The manic, debt-fueled nature of the advance suggests that China Evergrande, and China real estate in general, are in topping territory.”

What Happened Next?

Just three months later, the share price of Evergrande peaked and proceeded to fall an astounding 99%. By January 2025, China Evergrande’s shares had fallen from over $31 to just 16 cents.

Imagine if you had read our warning THREE MONTHS BEFORE THE TOP, in 2017. You would have been prepared for the stunning crash that followed.

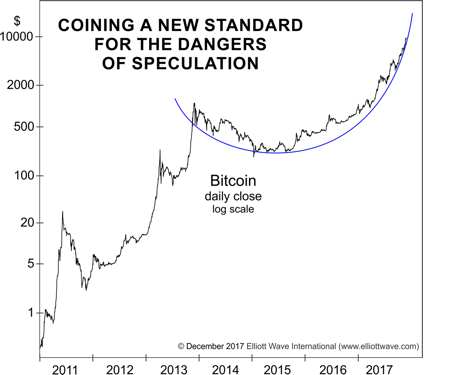

2017: Bitcoin Mania – The First Bubble

In December 2017, Bitcoin fever reached full-blown mania. Global media declared it “the future of money.” The launch of Bitcoin futures on the CME and CBOE was hailed as Wall Street’s stamp of approval. Here’s what Global Market Perspective said to subscribers:

Analysis/Forecast:

December 1, 2017:

“A market that looks and quacks like a bubble is a bubble. With a surge of 1130%, no market in history has bubbled the way bitcoin has over the past 11 months…

In a classic sign of a terminating mania, even the most novice of investors is now piling into bitcoin.”

Bitcoin’s rise from 2011 should eventually be followed by a clean break of the exponential curve drawn on the chart.

A breakdown from the bowl should lead to a bitcoin bear market…”

What Happened Next?

Bitcoin would hit its peak just 16 days later. A few days after that top, Elliott Prechter said in interview with Newsmax:

“I Wouldn’t Touch Bitcoin — Risk of Collapse Too Big.”

— Newsmax, December 21, 2017

Then, in early January 2018, our Global Market Perspective published a special section titled “Bitcoin: The Greatest Bubble of All Time” and said:

January 5, 2018:

“On December 1, GMP cited a ‘rising sea of euphoria, ever-higher price projections and the capitulation of financial sophisticates’ as a powerful combination of forces that would mark the demise of bitcoin’s incredible upward trajectory…

Is the bitcoin mania really over? The odds are high that it is…”

Overall, from it’s peak, Bitcoin plunged more than 80%, bottoming near $3,200 in December 2018.

By January 2019, the “crypto winter” narrative dominated — confirming the warnings EWI issued at the height of euphoria.

2020: The Fastest Bear Market in History

By late 2019 and early 2020, optimism toward stocks had reached euphoric extremes. Major indexes pushed to record highs as headlines declared the bull market “unstoppable,” fueled by Fed rate cuts and trade-deal hopes. Retail speculation surged to manic levels, daily trading hit records, and Gallup’s “Mood of the Nation” showed personal satisfaction at a 40-year high while concern about the economy fell to its lowest level in decades — classic signs of sentiment near a historic extreme.

Analysis/Forecast:

October 2019:

“A major divergence between recent highs in three major U.S. stock indexes — the Dow Industrials, the S&P 500 and the NASDAQ Composite — as well as various laggards such as the Dow Jones Transportation Average and the S&P Small Cap 600 Index … is a precursor to a significant stock market decline.”

November 2019:

“A record net-short position in futures contracts by Large Speculators on the CBOE Volatility Index (VIX) suggests that an upcoming spike in volatility will wipe away the calm veneer.”

February 7, 2020:

“The Great Bull Market has become so entrenched that pundits use words such as raging and relentless to describe it (CNBC, January 18). One pundit projected a January rise and then an accompanying rally through the remainder of the year based on historical precedent. With a late January swoon, however, the Dow Jones Industrial Average began the year with a down month. It is a small hint at what we view as strong potential for a bearish surprise in 2020.”

February 21, 2020

“The S&P 500 appears to have completed wave 5 at 3393.52, the high on February 19. The decline to 3328.60, a low this afternoon, may be labeled as five waves. This impulse pattern is wave i of a larger five-wave declining structure. Wave ii will be a snapback rally that will likely last 1-3 days. When complete, the index will start wave iii down. … The other option is that a series of first and second waves have developed since the high, which implies acceleration of the declining trend next week. The recent highs on February 12-19 (Dow and S&P) are now a key level for the bearish case.”

February 24, 2020:

“Various news stories in print and on TV proffered myriad explanations for today’s selloff — Coronavirus, outbreaks in Italy, China’s economic slowdown, outbreaks in South Korea, weak potential for companies doing business in Asia, etc. — but none stand up to reality. All these supposed causes have been well known prior to today. The reason the market accelerated its decline is because it was at the point in the progression of its Elliott wave pattern that indicated a sharp drop.”

What Happened Next?

The Dow peaked February 12 at 29,568 and the S&P 500 followed February 19 at 3393.

In only seven trading days, the S&P fell 16 percent — the fastest drop from an all-time high in history — and in five weeks, major indexes were down more than 35 percent.

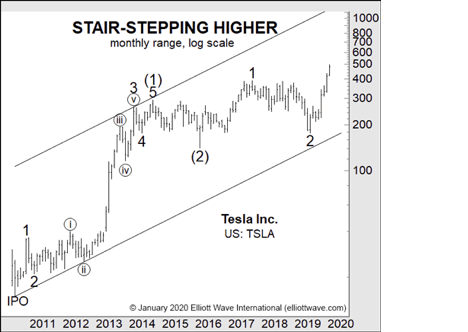

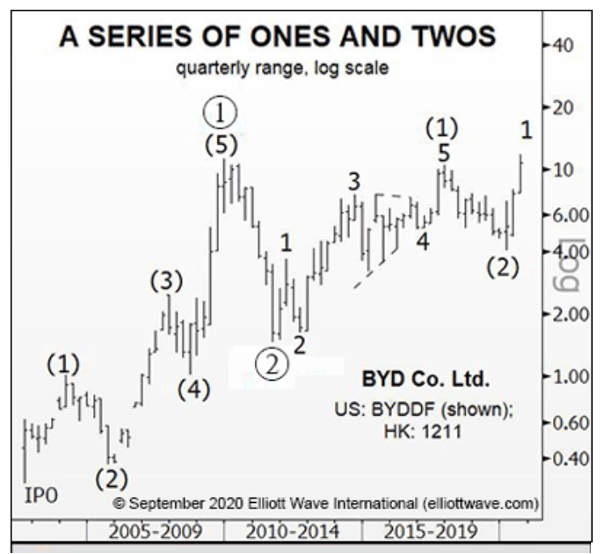

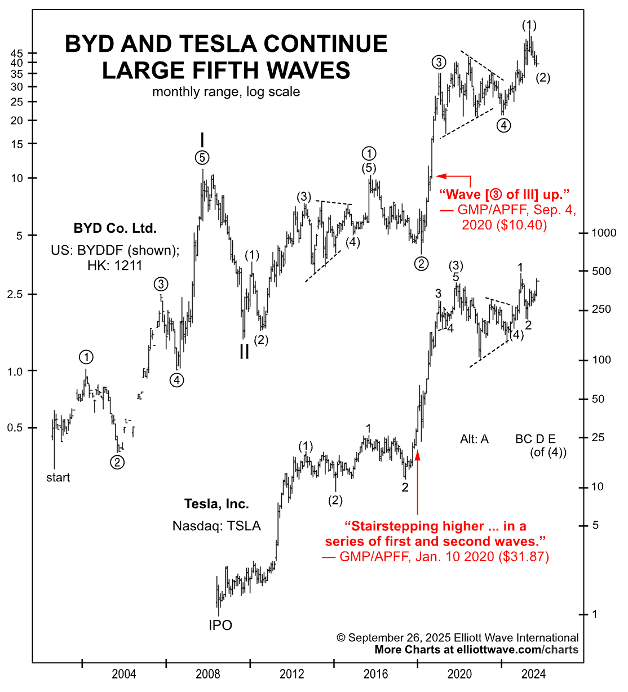

2020: TESLA & BYD

In early 2020, optimism toward electric vehicle (EV) stocks was just beginning to accelerate. Tesla had recently broken above $30 per share (split-adjusted) amid growing excitement over its inclusion in major indexes and record deliveries. BYD shares, meanwhile, were still trading near $10 as China’s EV industry was recovering from a slump in 2019.

Analysis/Forecast:

January 10, 2020:

Tesla Inc.:

“Stair-stepping higher … in a series of first and second waves.”

September 4, 2020:

“BYD Co. Ltd. recently broke out above long-term resistance near $10 (HK $84) in wave (3) of 3 up, which implies considerable upside in coming years.”

What happened next?

Tesla’s advance went vertical through 2020, gaining more than 700% by year-end and achieving a market cap above $800 billion by early 2021.

BYD surged from roughly $10 to above $40, later becoming one of the world’s largest EV manufacturers by sales.

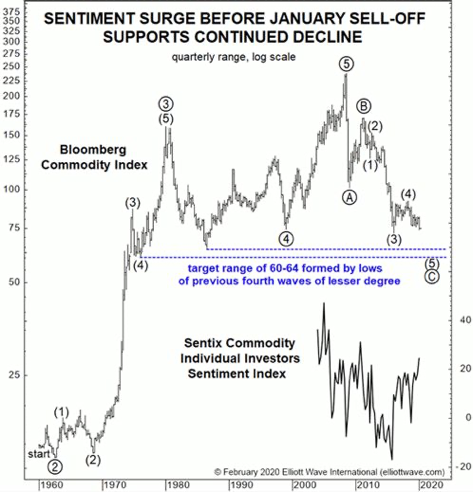

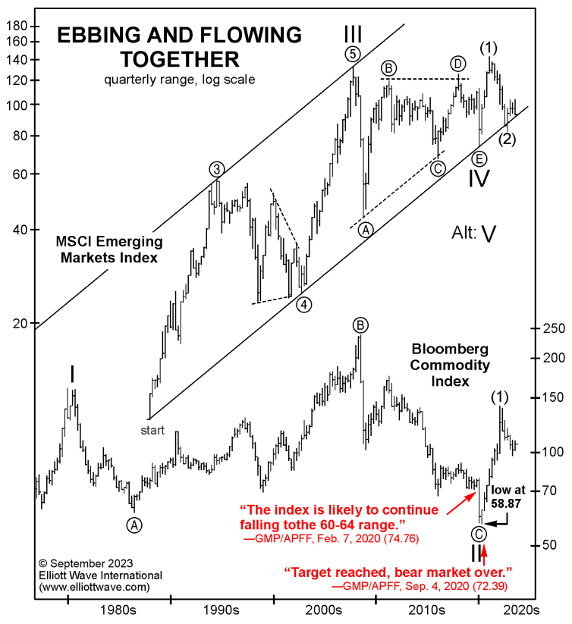

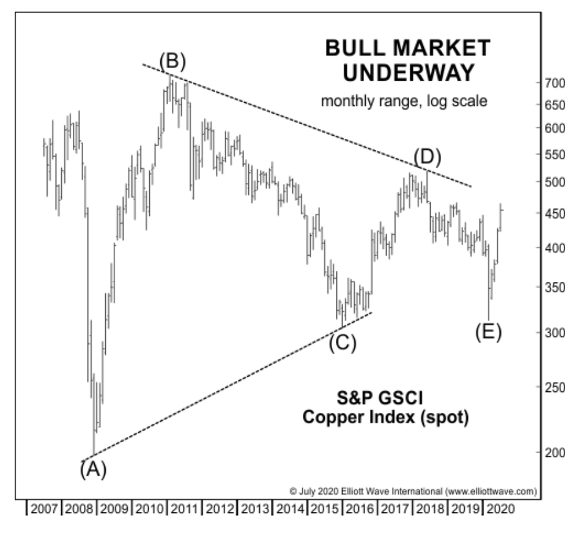

2020: Commodities: “Target Reached, bear market over.”

By early 2020, commodities had been in a 12-year secular bear market since 2008. Prices were depressed across metals, energy, and agricultural goods. Sentiment was overwhelmingly negative as global disinflation and low interest rates persisted. The Bloomberg Commodity Index hovered near multi-decade lows, and investors viewed commodities as a stagnant asset class compared with booming equities and technology shares.

Analysis/Forecasts:

February 7, 2020:

“The [Bloomberg] commodity index is likely to continue falling at least 15–20% to the 60–64 range — which represents the lows of previous fourth waves of lesser degree, where corrections often end…. We can see sentiment support for continued decline… which suggests that commodities are sliding down a slope of hope.”

Two months later, the index bottomed less than 2% below that target range.

September 2020:

“Target reached … bear market over.”

“Commodities overall have also ended their secular bear market from 2008.”

What happened next:

After September 2020, the Bloomberg Commodity Index began a broad, sustained advance led by copper, energy, and agricultural prices. By mid-2021, the index had surged more than 60% from its low, confirming that a major trend reversal had taken place.

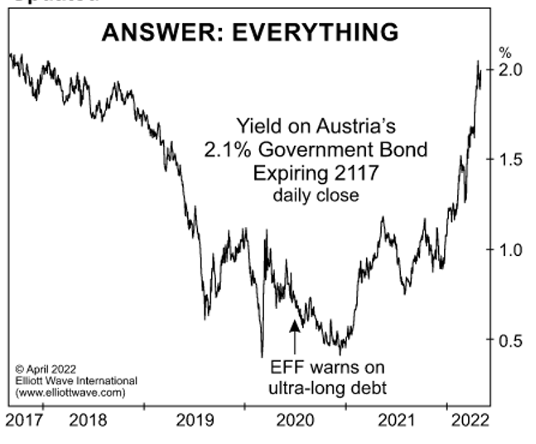

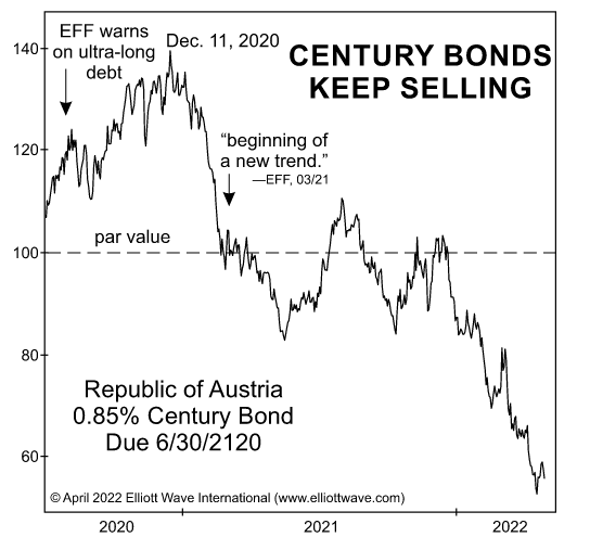

2020: Austria’s Century Bond

By mid-2020, global interest rates had plunged to record lows. Investors, desperate for yield, piled into long-dated government bonds — some stretching out 100 years — betting that rates would stay near zero indefinitely. In March 2020, the yield on Austria’s 2117 century bond fell below 0.5%, and demand remained overwhelming: when the government issued another €2 billion tranche paying just 0.88%, orders totaled eight times the available supply. Pension funds and insurers saw these ultra-long maturities as “safe” yield plays in a world awash with negative rates.

Analysis/Forecast:

Global Market Perspective – July 2, 2020:

“Credit ‘investors’ are loading up on the most highly leveraged bonds, betting that current market trends will continue and interest rates will keep falling. … For century bonds, the duration risk is so high that even a tiny upward blip in interest rates can send the bond price tumbling. So far, investors have ignored the mounting risk…”

What Happened Next?

As global inflation accelerated and interest rates began to rise in 2021–2022, Austria’s century bond collapsed. By 2023, Bloomberg reported:

“Austria’s Century Bonds Have Cost Investors Dearly.”

Prices of the 2117 bond fell more than 70% from their 2020 highs, making it one of the worst-performing sovereign bonds in history.

What had been hailed as a safe, long-term investment became a textbook example of how duration risk can devastate portfolios when interest-rate trends reverse.

2020: The Rise of Copper

Sentiment toward commodities was deeply bearish following the selloff. By March 2020, copper had plunged to a four-year low, with investors convinced that a prolonged global recession was just beginning.

Analysis/Forecast:

July 31, 2020:

“The completed triangle pattern in copper indicates that a massive bull market is already underway.”

What happened next?

After July 2020, copper prices accelerated sharply. Within ten months, the metal doubled, reaching its highest level in a decade by May 2021. The rally confirmed that the massive new bull market was indeed underway, with copper becoming one of the leaders of the global commodity boom that followed. By early 2022, copper had gained over 150% from its 2020 lows — precisely the kind of explosive move the wave pattern anticipated.

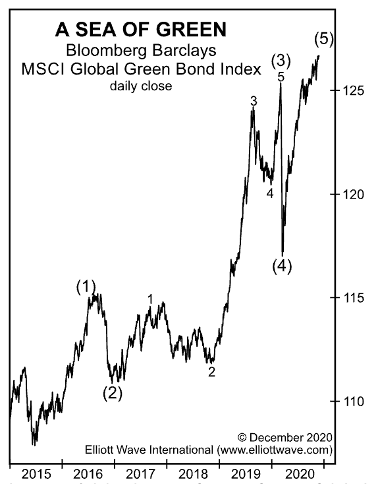

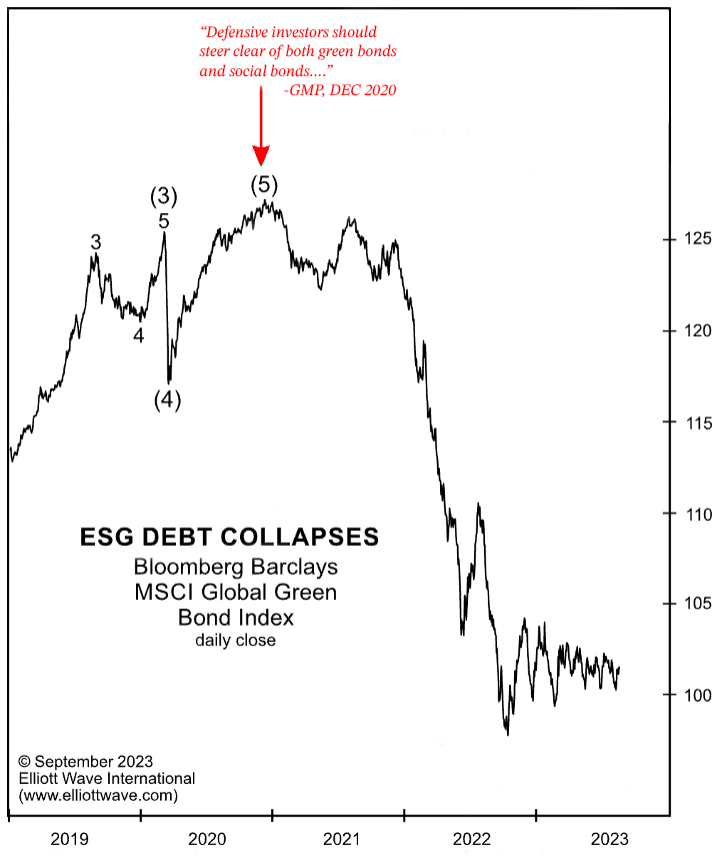

2020: Green and Social Bonds: A New Kind of Euphoria

By late 2020, investor enthusiasm for green and social bonds reached record levels. With global interest rates near zero and central banks flooding markets with liquidity, demand for new types of debt surged. The Bloomberg Barclays MSCI Global Green Bond Index hit a new all-time high as the market for funds with environmental, social and governance (ESG) mandates grew 170% since 2015, and the total amount of euro-area green bonds outstanding rose sevenfold.

Governments joined the wave: in October 2020, the European Commission issued €17 billion in “social bonds” — the largest supranational transaction in history — to fund pandemic relief through the EU’s SURE program. A month later, UK Chancellor Rishi Sunak announced plans for “green gilts” to boost Britain’s post-Brexit environmental credentials. Analysts called it “a major leap into the global debt big leagues.”

Analysis/Forecast:

December 2020:

“The sudden appearance of, and seemingly insatiable demand for, new types of debt is another telltale sign of dangerous credit-market complacency.”

“Investors’ risk tolerance for new forms of debt has risen cavalierly alongside global stocks. Today, experts have loudly proclaimed that so-called social bonds will be the next great innovation, but the euphoria surrounding this new debt is actually one of the biggest reasons to remain skeptical. As we have discussed for months, low interest rates have pushed desperate investors to buy debt from weaker borrowers (exposing them to nonpayment) or to buy longer-dated debt (exposing them to rising interest rates). Social bonds offer the worst of both worlds. Not only was the debt issued in maturities of 10 and 20 years — far too long for defensive investors to tie up their money — but both maturities pay higher returns than the benchmark German bund.”

“Defensive investors should steer clear of both green bonds and social bonds…. When social mood waxes negative, even the most socially conscious investors will sell these bonds indiscriminately.”

What happened next?

As global interest rates rose sharply beginning in 2021, the value of long-dated ESG bonds plunged alongside broader fixed-income markets. By 2022–2023, investors suffered steep mark-to-market losses.

The once-celebrated “next great innovation” in credit markets became another example of late-cycle excess — a warning that even debt tied to noble causes is not immune to the forces of social mood and market reversal.

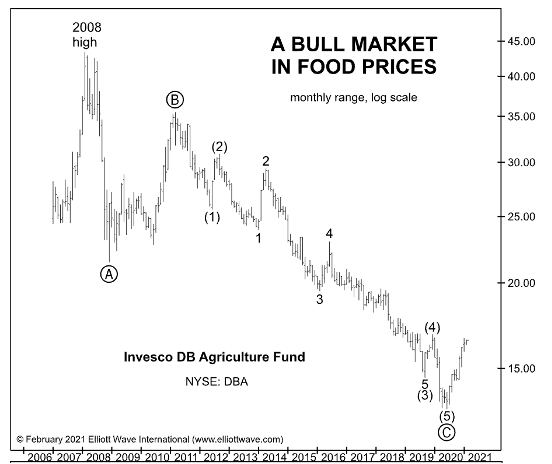

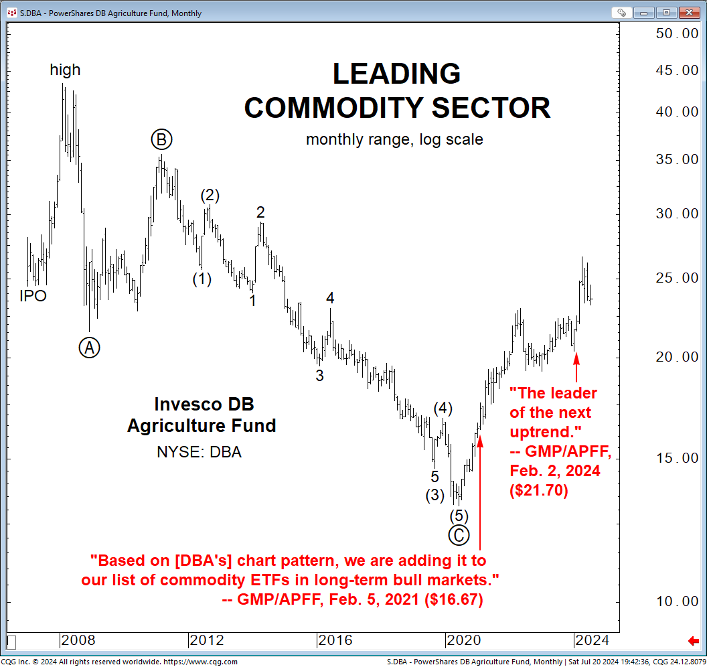

2021: Agriculture – The Leader of the Next Commodity Uptrend

Throughout the late 2010s, agricultural commodities lagged behind other markets. Years of oversupply, trade disruptions, and weak investor sentiment had left the sector deeply depressed. By early 2021, the Invesco DB Agriculture Fund (DBA) — a broad agricultural commodity ETF — had fallen to levels not seen in more than a decade. Most analysts viewed it as “dead money,” assuming the multi-year downtrend would continue indefinitely.

Forecast/Analysis:

February 5, 2021:

“Based on [DBA’s] chart pattern, we are adding it to our list of commodity ETFs in long-term bull markets.”

What happened Next:

From its 2020 low near $14, DBA began a sustained advance. In February 2024, GMP reaffirmed the fund’s position, calling it “The leader of the next uptrend”.

The fund continued to rise above $25, a gain of more than 70% from its 2020 low, confirming its emergence as one of the strongest performers in the commodities complex.

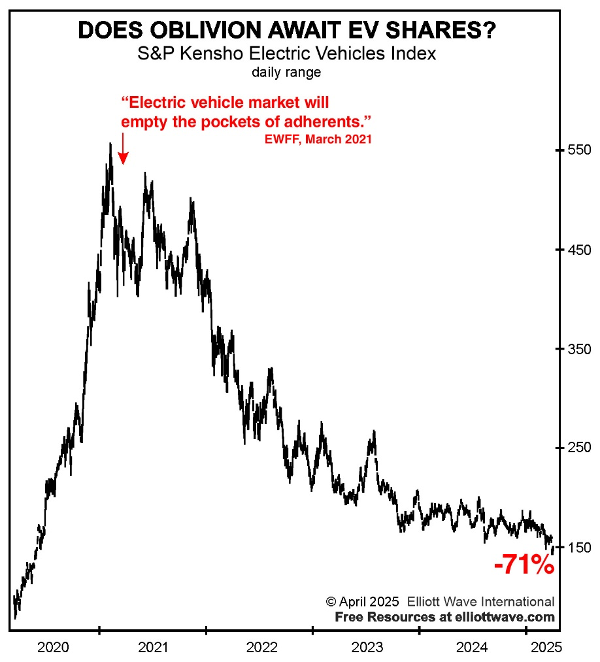

2021: Electric Vehicles: The Green “Money Machine” Peaks

In 2020 and early 2021, enthusiasm for electric vehicles (EVs) surged to speculative extremes. The sector became the centerpiece of the global “green tech” boom as investors poured into EV manufacturers, battery producers, and charging infrastructure firms.

The S&P Kensho Electric Vehicles Index skyrocketed nearly fivefold from March 2020 to February 2021, fueled by stimulus money, ESG fund inflows, and widespread belief that EVs represented a once-in-a-generation transformation of the auto industry.

Analysis/Forecast:

March 2021:

“The electric vehicle market is another green ‘money machine’ that will ultimately empty the pockets of adherents.”

What Happened Next?

The S&P Kensho Electric Vehicles Index peaked in early 2021 and entered a prolonged decline. Over the next four years, the index plunged 71%, erasing nearly all of its gains from the 2020–2021 boom. Once heralded as the future of transportation, EV shares became another case study in speculative excess.

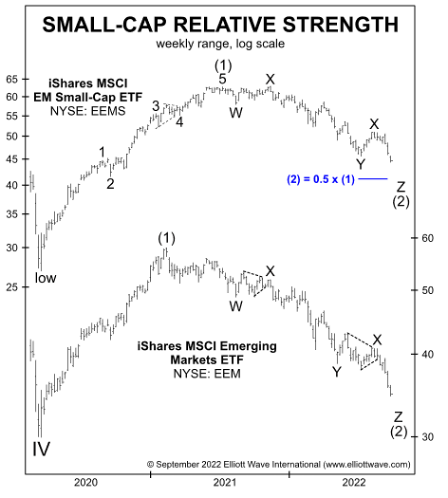

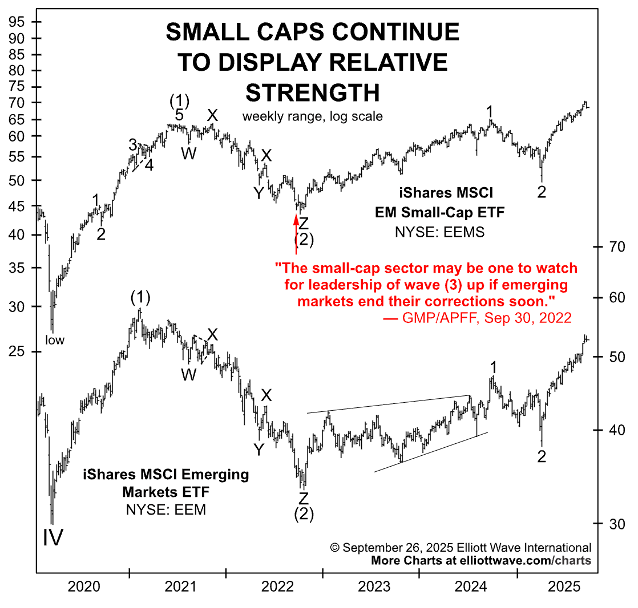

2022: Emerging Market Small Caps: Quiet Strength Beneath the Surface

By late 2022, emerging market equities had endured a prolonged decline. The iShares MSCI Emerging Markets ETF (EEM) had fallen. Investor sentiment toward developing economies was deeply negative, with capital flowing back toward the U.S. and Europe.

Analysis/Forecast:

September 30, 2022:

“The small-cap sector may be one to watch for leadership of wave (3) up if emerging markets end their corrections soon.”

What Happened Next?

Following the September 2022 forecast, emerging market small caps climbed steadily, gaining more than 30% by September 2025.

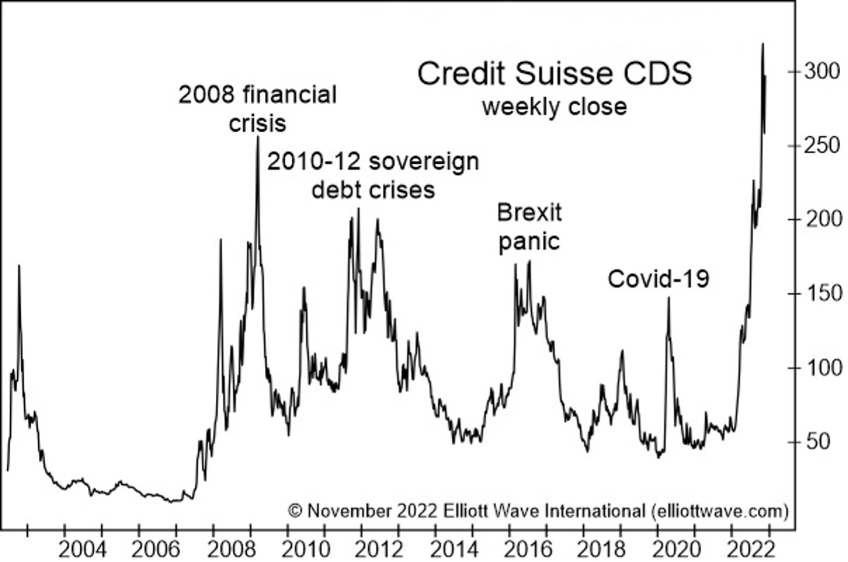

2022: Credit Suisse CDS

By late 2022, cracks were appearing in the global banking system. Decades of easy credit and aggressive lending had left many financial institutions vulnerable to tightening liquidity and falling asset prices. In October, Credit Suisse, one of Europe’s oldest and most prestigious banks, faced intensifying scrutiny as concerns about its stability spread through markets.

Forecast/Analysis:

November 4, 2022:

“Just last month, Credit Suisse — the once-venerable Zurich-based global investment bank that GMP has warned about for years — saw prices for its credit-default swaps (CDS) shoot past 300, indicating investors’ increasing belief that the bank will default. As shown, CDS prices have exceeded every high-water mark set during every crisis of the past 15 years.”

What happened next?

Within four months, the warning was realized. In March 2023, Credit Suisse collapsed after massive depositor flight and a loss of confidence in its solvency. As CNN reported in April 2023:

“Depositors pulled $75 billion from Credit Suisse as it veered toward collapse.”

Credit Suisse was sold to UBS for $3.25 billion, marking one of the most dramatic banking failures in modern European history. What began as a subtle warning in the credit markets — captured by our analysis months earlier — became a full-scale crisis that reshaped the global banking landscape.

2024: Xiami Corp.

In the April 2024 issue of Global Market Perspective, EWI Chief Asian and Emerging Markets Analyst Mark Galasiewski spotted a completed expanded flat pattern (highlighted in red on the chart below) in an Emerging Market Leader, Xiaomi Corp. He alerted his subscribers to the bullish setup:

Analysis/Forecast:

“We think that the company’s shares completed a flat correction from their 2018 IPO to a low in October 2022 and since then are tracing out a series of first and second waves in a new impulsive advance.“

What Happened Next?

Xiaomi Corp. QUADRUPLED in a year!

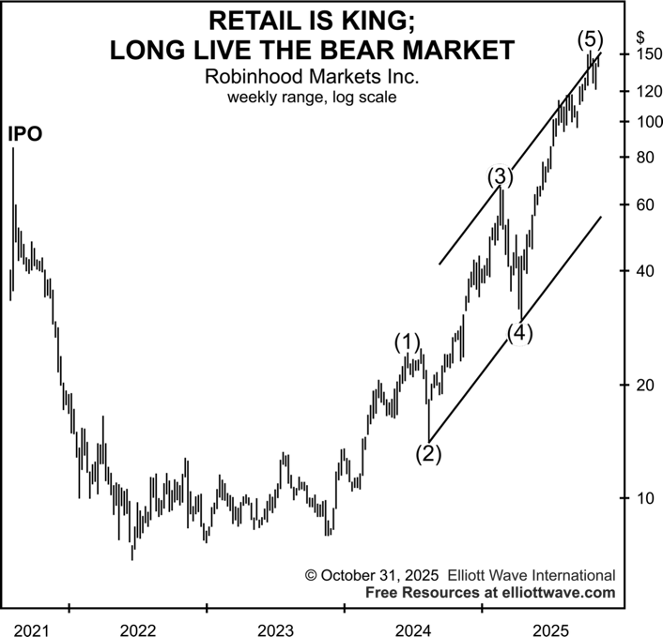

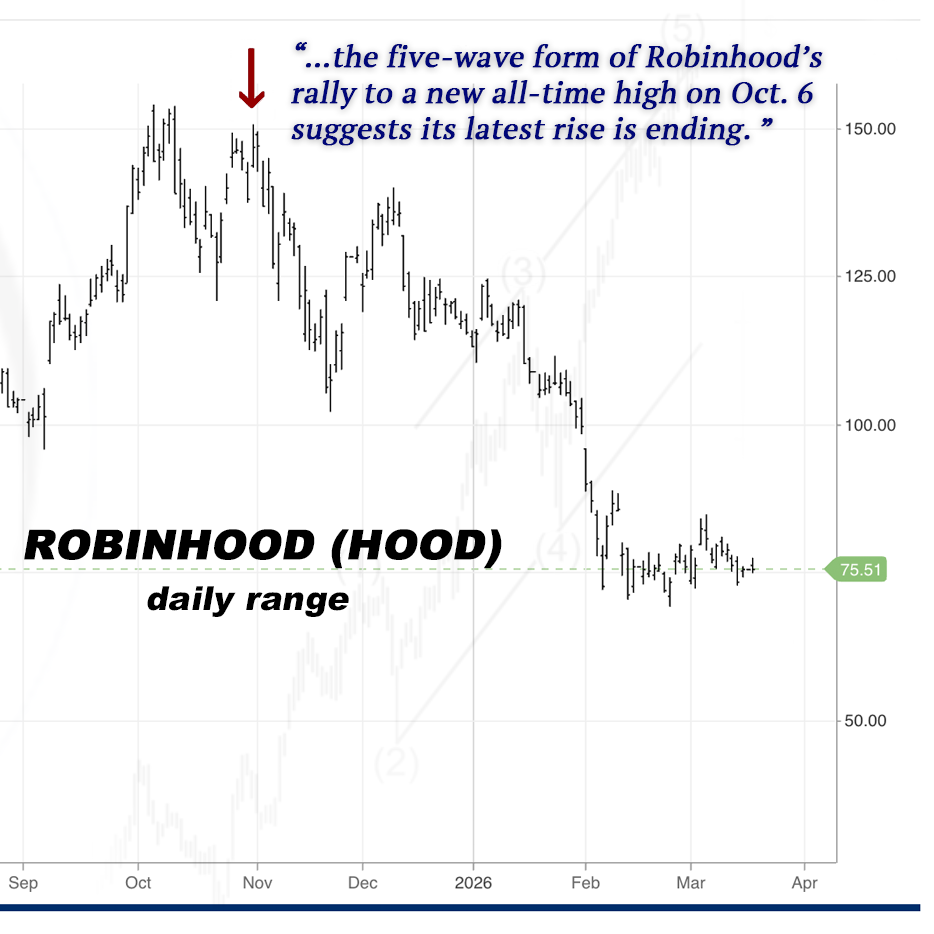

2025: Robinhood Markets Inc. (HOOD)

As optimism toward the Robinhood Markets Inc. (HOOD) stock reached a new extreme, analysis from our Global Market Perspective identified signs that the rally was likely nearing completion.

Analysis/Forecast:

October 31, 2025:

“…the five-wave form of Robinhood’s rally to a new all-time high on October 6 suggests its latest rise is ending. King Retail should quickly celebrate its latest position on top because it is all about to change.”

What Happened Next?

The warning proved timely:

By February 24, 2026, HOOD had declined to an intraday low of $69.22 — a drop of roughly 55% from the October peak.

See How Some Subscribers Use Global Market Perspective

What Do I Get With A Subscription?

Immediate access to the latest issues, so you can get up to speed quickly. From there, you’ll be notified whenever a new issue or update is published.

You also get access to “Subscriber Extras” and free educational materials including: books, reports, videos and free or discounted trials of our other services that you may find valuable.

How is Delivered?

All publications and resources are delivered online through our MyEWI Subscriber Portal. Just sign-in through your computer, phone or tablet for instant access. Here are some photos of what it looks like:

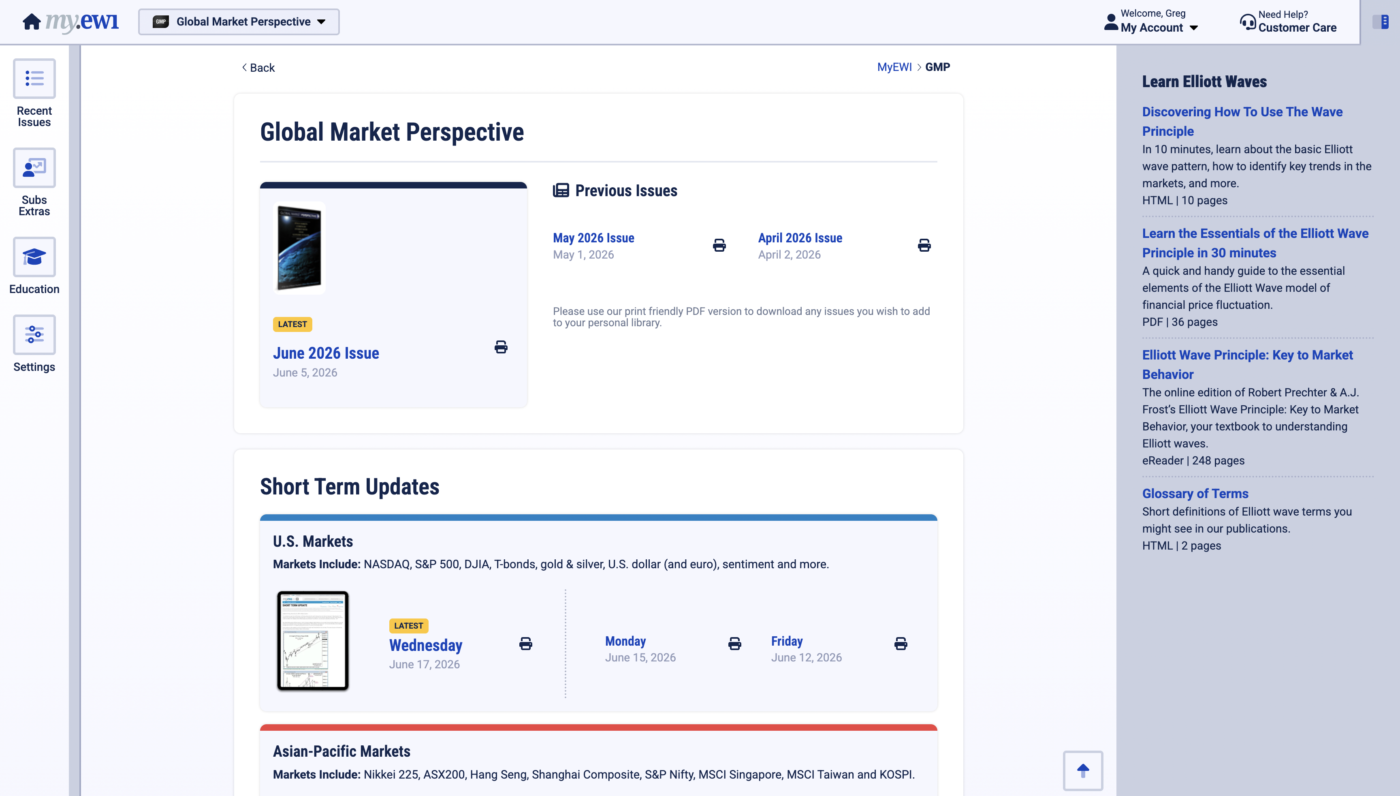

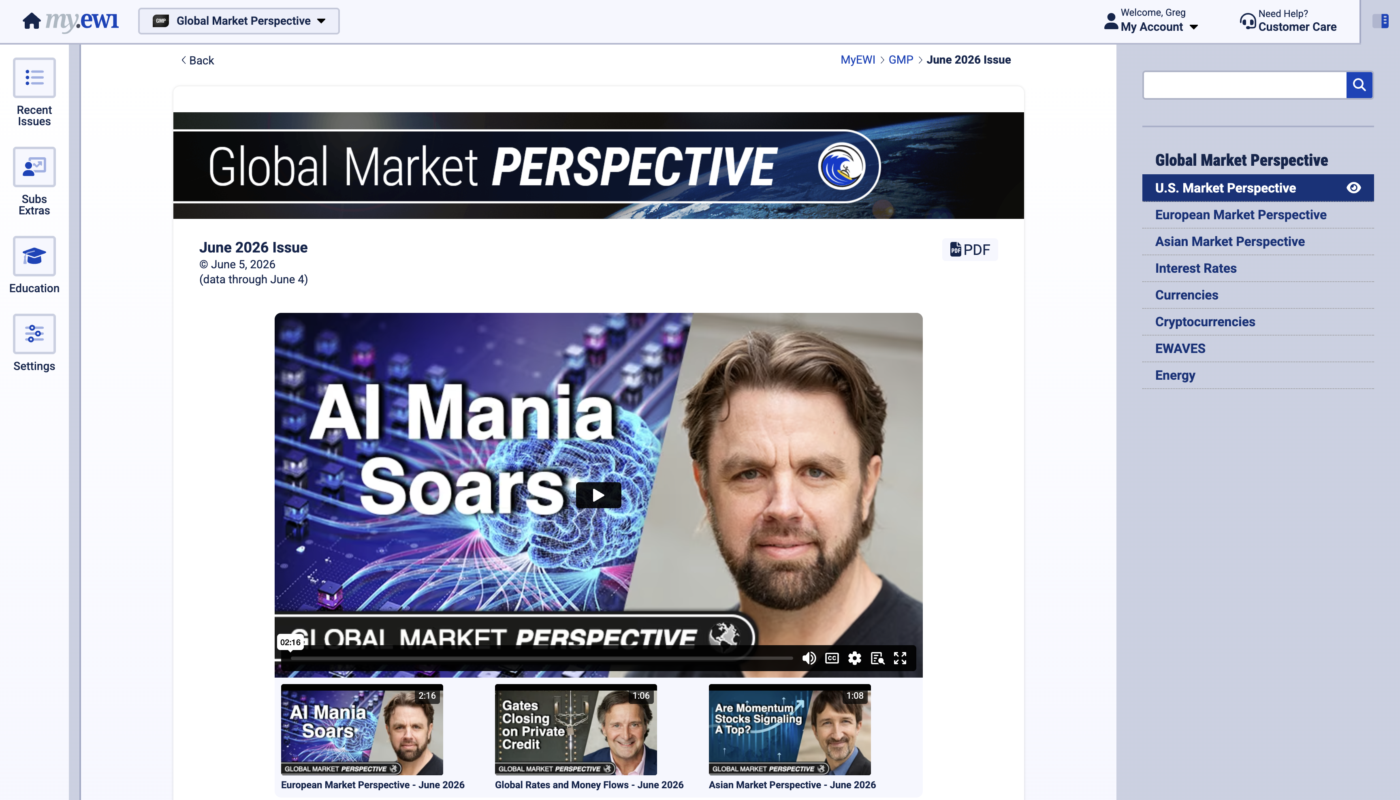

The MyEWI Home Dashboard – To Access All Your Subscriptions & Resources

Global Market Perspective Subscription Portal

All issues of your subscription can be viewed instantly online via computer, phone and/or tablet.

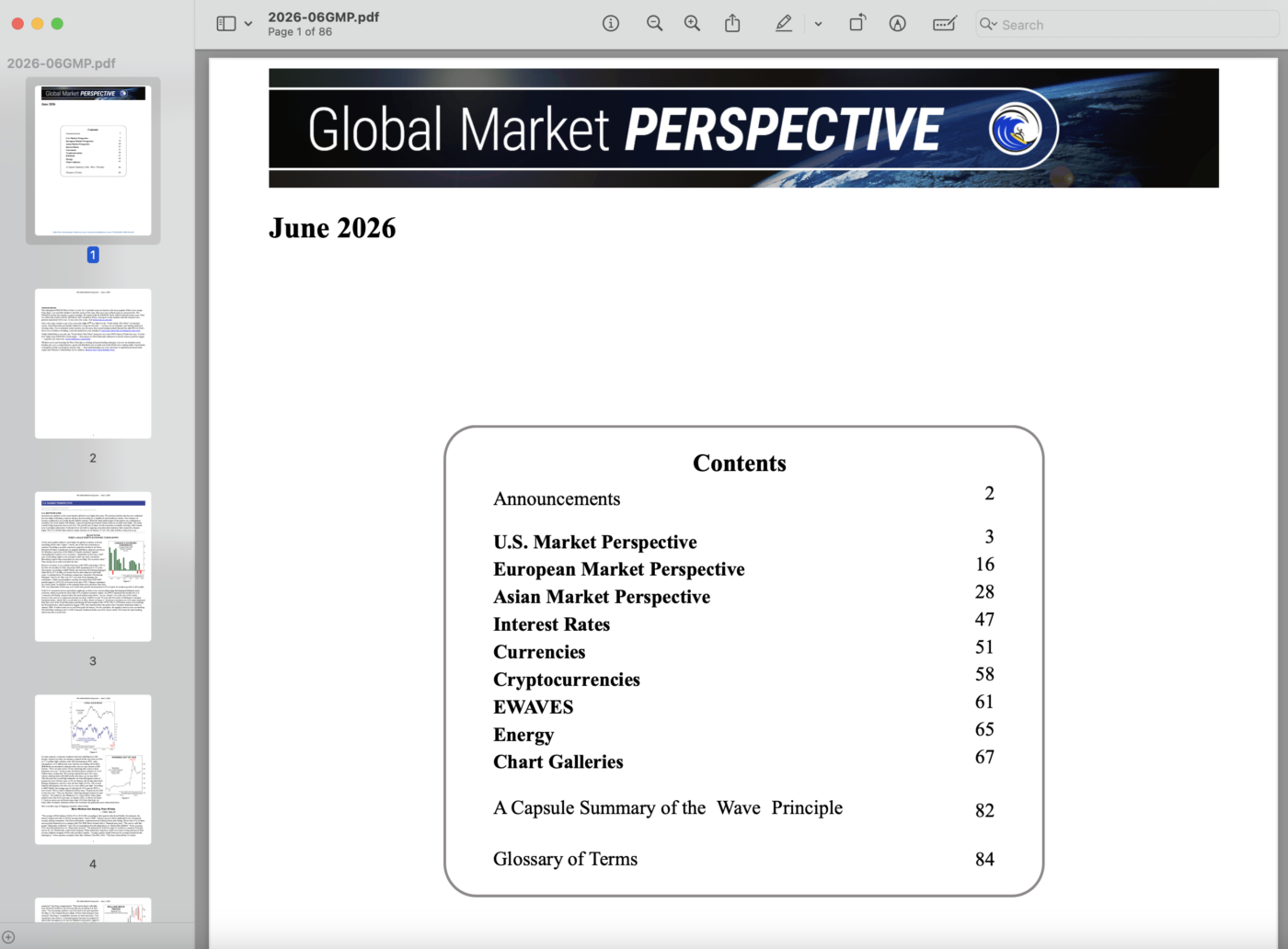

You can also download and print your issues, if you would like to read them that way.

All subscriptions come with Free Educational Materials & Resources

“Subscriber Extras” vary depending on your subscription and update regularly.

To Subscribe, Choose Your Option Below:

Global Market Perspective

Global Market Perspective

(Just get this essential monthly publication covering 50+ global markets)

Choose your billing frequency:

Monthly

$77/mo

Annual

$924/yr

Need more active global market updates?

Add a regional, three-times-a-week Short Term Update

Our Short Term Updates deliver detailed, near-term analysis of key markets in their region 3x a week. Each update provides clear, objective forecasts and analysis—complete with Elliott wave-labeled charts—showing you exactly where we believe the markets are headed in the days and weeks ahead.

Most Popular: Get GMP + U.S. Short Term Update

(Short term coverage includes: NASDAQ, S&P 500, DJIA, T-bonds, gold & silver, U.S. dollar (and euro), sentiment and more.)

Choose your billing frequency:

Monthly

$144/mo $117/mo

Annual

$1,728/yr $1,404/yr

(You save 18%)

Get GMP + Asian-Pacific Short Term Update

(Short term coverage includes: Nikkei 225, ASX200, Hang Seng, Shanghai Composite, S&P Nifty, MSCI Singapore, MSCI Taiwan and KOSPI.)

Choose your billing frequency:

Monthly

$144/mo $117/mo

Annual

$1,728/yr $1,404/yr

(You save 18%)

Get GMP + European Short Term Update

(Short term coverage includes: DAX, FTSE, CAC-40, Euro Stoxx 50, Bunds, euro and other featured markets across Europe.)

Choose your billing frequency:

Monthly

$144/mo $117/mo

Annual

$1,728/yr $1,404/yr

(You save 18%)

*If you’d like to get GMP + 2 or all 3 Short Term Updates contact customer care for your special discounted rates.

Not ready to subscribe to GMP? Try a single issue >>

Order by Phone

Mon-Fri, 8am-5pm Et

Contact us at 800-336-1618 or 770-536-0309 (Internationally) and you will get a fast, friendly, knowledgeable person to assist you.

LIVE CHAT

Mon-Fri, 8am-5pm ET

Please use the LIVE CHAT button at the bottom right of your screen to chat with us.

We accept online payments from Visa, MasterCard, American Express, Discover, and Bitcoin through our online store. We also accept payment via PayPal, money order, bank wire, and check (drawn off a U.S. bank). If you would like to pay by any of these methods, please contact our Customer Care Representatives via phone, email, or live chat to place your order.

Enhanced Global Coverage Options:

1) If you want intensive coverage of the U.S., European or Asian stock markets, as well as currencies, commodities, cryptocurrencies and energy markets, you need our Pro Services.

2) For Indian market coverage only: Click Here >>

EWI’s Research is Trusted by Thousands of Independent Investors and Market Professionals at the World’s Largest Institutions