It’s Earnings Season! Up is Good and Down is Bad, Right?

Every quarter, the mainstream media is full of headlines that spew the so-called “conventional wisdom” that good earnings equate to higher stock prices and poor earnings to lower prices.

Let’s see how that’s working out!

This morning, Intel announced weak quarterly earnings and the stock opened down 9%. OK, so that one makes sense.

BUT, at the same time, Amex announced that it missed profit estimates in Q4 and the stock traded….up 10%???

Wait, what? Seems like we might need some extra “guidance” on that one!

Robert Prechter, in The Socionomic Theory of Finance, has this to say:

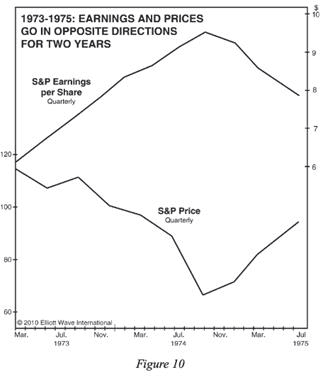

Suppose you knew that corporate earnings would rise strongly for the next six quarters straight. Would you buy stocks? Figure 10 shows that in 1973-1974, earnings per share for S&P 500 companies soared for six quarters in a row, during which time the same companies’ stock prices suffered their largest collapse since 1937-1942. This is not a small departure from the expected relationship but a history-making departure. Moreover, the S&P bottomed in early October 1974, and earnings per share then turned down for twelve straight months, just as the S&P turned up! A speculator with foreknowledge of these earnings trends would have made two perfectly incorrect decisions, buying near the top of the market and selling at the bottom. Such glaring exceptions to the idea of a causal relationship between corporate earnings and stock prices pose a challenge for conventional economic theory.

In real life, no one knows what earnings will do, so no one would have made such bad decisions on the basis of foreknowledge. Unfortunately, the basis that investors actually use is estimated earnings, which incorporate analysts’ lagging trend-extrapolation bias (see Chapters 17 and 21), making their investment decisions often even worse timed than advance knowledge of earnings would allow.